Several weeks ago President Obama gave his State of the Union speech and according to him all is hunky-dory. He touted the fastest growing economy since the tech boom, the strongest labor market since 1999, and shrinking deficits for the first time since the Great Recession.

Either Obama is living in a different world than everybody else or he’s a blatant liar.

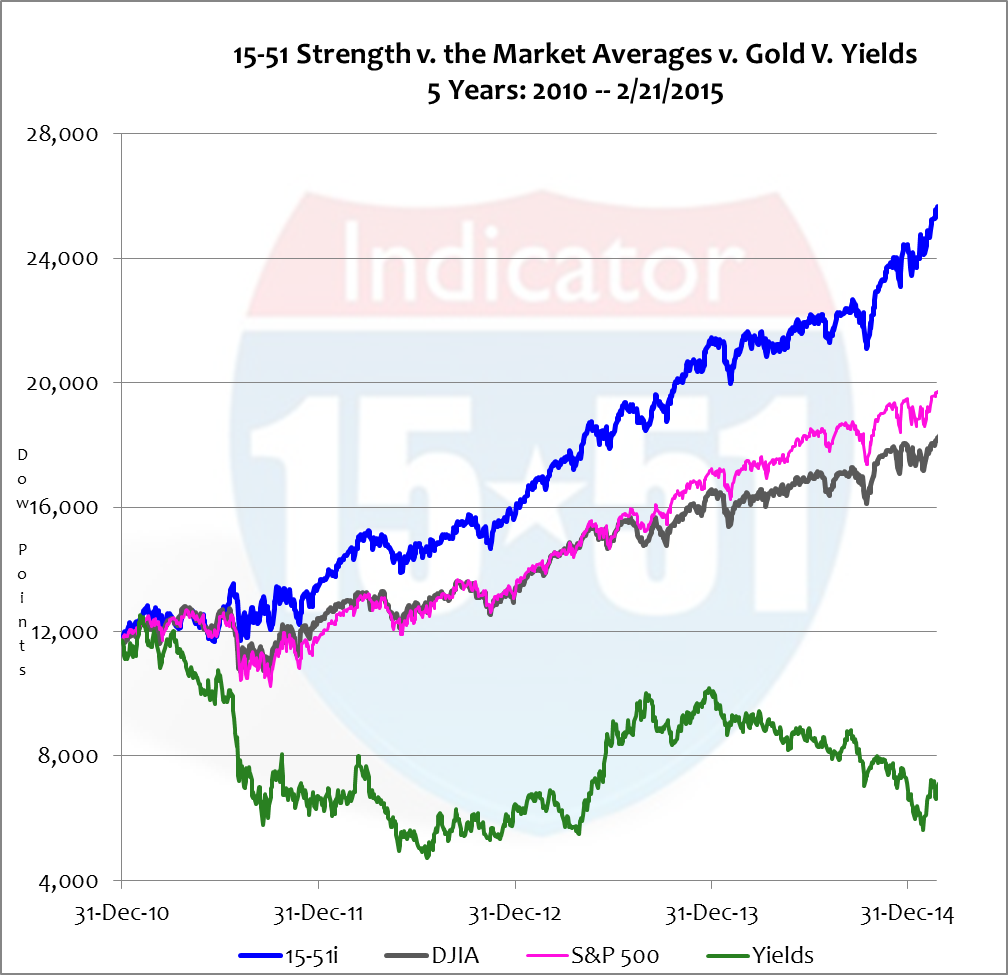

Truth be told, this year Obama’s budget will produce $100 billion more in deficit than last year’s did; labor participation is at the lowest level since Carter’s market in 1978; and Clinton’s tech-boom economy averaged 6.1% growth while Obama’s economy is averaging just 2.9% – and if the economy was as strong as Obama portrays, then yields would be 6%, not 2%.

The reason yields aren’t that high is because there’s too much demand for U.S. Treasury Securities – at 2% interest, mind you. Think about that for a second. In this stock market (see below) demand for low-risk low-reward bonds is booming.

Stock market strength has gained 95% since the economy was levered out of recession, and the Dow Average has added 55%. Yet yields have fallen 36% in the same time. Indeed, QE had a very strong hand in that drop. But what about now? Why hasn’t the elimination of QE forced yields higher? And if the economy is as good as Obama says, and clear waters are ahead, then why are so many investors willing to earn 2% in bonds while the stock market is “roaring ahead.”

Because institutional investors are running scared to safety (U.S. Treasuries).

In strong economic environments yields rise to entice investors to shift capital from higher returning stocks to the bond market. During the tech-boom expansion, for instance, the 10 yield was routinely above 6% – a far cry from today’s meager 2% mark.

Yields are telling the story of economic weakness and global uncertainty, and stocks are telling the opposite story.

Which is accurate?

For the answer to that let’s go to the hard facts. After posting two strong periods of economic growth in the 2nd and 3rd quarters, the pace for U.S. growth was cut in half in the holiday driven 4th quarter — and the economy experienced price deflation. In other words, retailers had to cut prices during the strongest quarter of the year to entice consumers to spend modestly.

That’s not a sign of strength.

Neither are these Wall Street Journal headlines:

- Hiring Booms, but Soft Wages Linger (1/9/2015)

- U.S. Retail Sales Reflect Consumer Caution Despite Lower Gas Prices (1/14/2015)

- WSJ Survey: Economists See 2015 GDP Growth at 3% (1/15/2015)

- U.S. Economic Growth Slows to 2.6% in Final Months of 2014 (1/30/2015)

- Jobs Report: U.S. Adds 257,000 Jobs; Unemployment Ticks Up to 5.7% (2/6/2015)

- Fannie, Freddie Weak Earnings Raise Possibility of Future Bailouts (2/20/2015)

And from across the pond…

- ECB Unveils Stimulus to Boost Economy (1/22/2015)

- China Injects $8 Billion into Banking System (1/22/2015)

- Bank of Russia Cuts Interest Rates (1/30/2015)

- Japan Escapes Recession but Growth Misses Forecasts (2/16/2015)

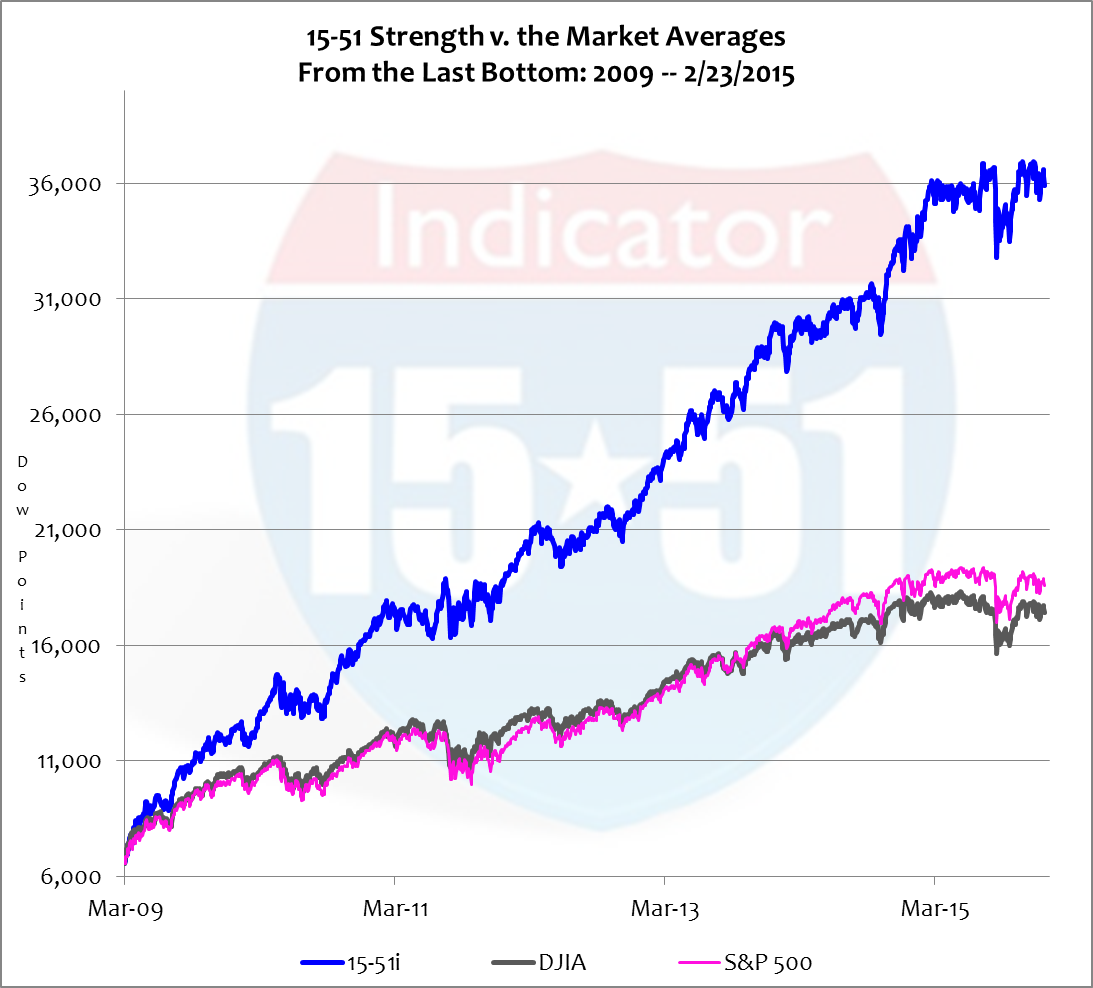

Add that to the turmoil in the Middle East and Ukraine and it’s hard to believe stocks are at all-time highs, again. The Dow closed the week at 18,140 and 15-51 strength closed at a new record, 87,777. Stock market strength is up more than 500% since the ’09 bottom, when it traded at 17,398 (just 700 points off the Dow’s current valuation.) See below.

The exceptional rise in stocks is unprecedented and unwarranted, which makes for a steeper correction next time around.

Stay tuned…

![]()